Keep Or Shred? The Paper Trail Playbook

03-23-2026

By Steve Gibson

Knowing which documents to hold onto and which ones to destroy isn't just about tidiness. It's about protecting yourself, staying prepared for life's curveballs, and making sure the paperwork that matters is easy to find when you need it most.

Here's a practical breakdown to help you sort it all out.

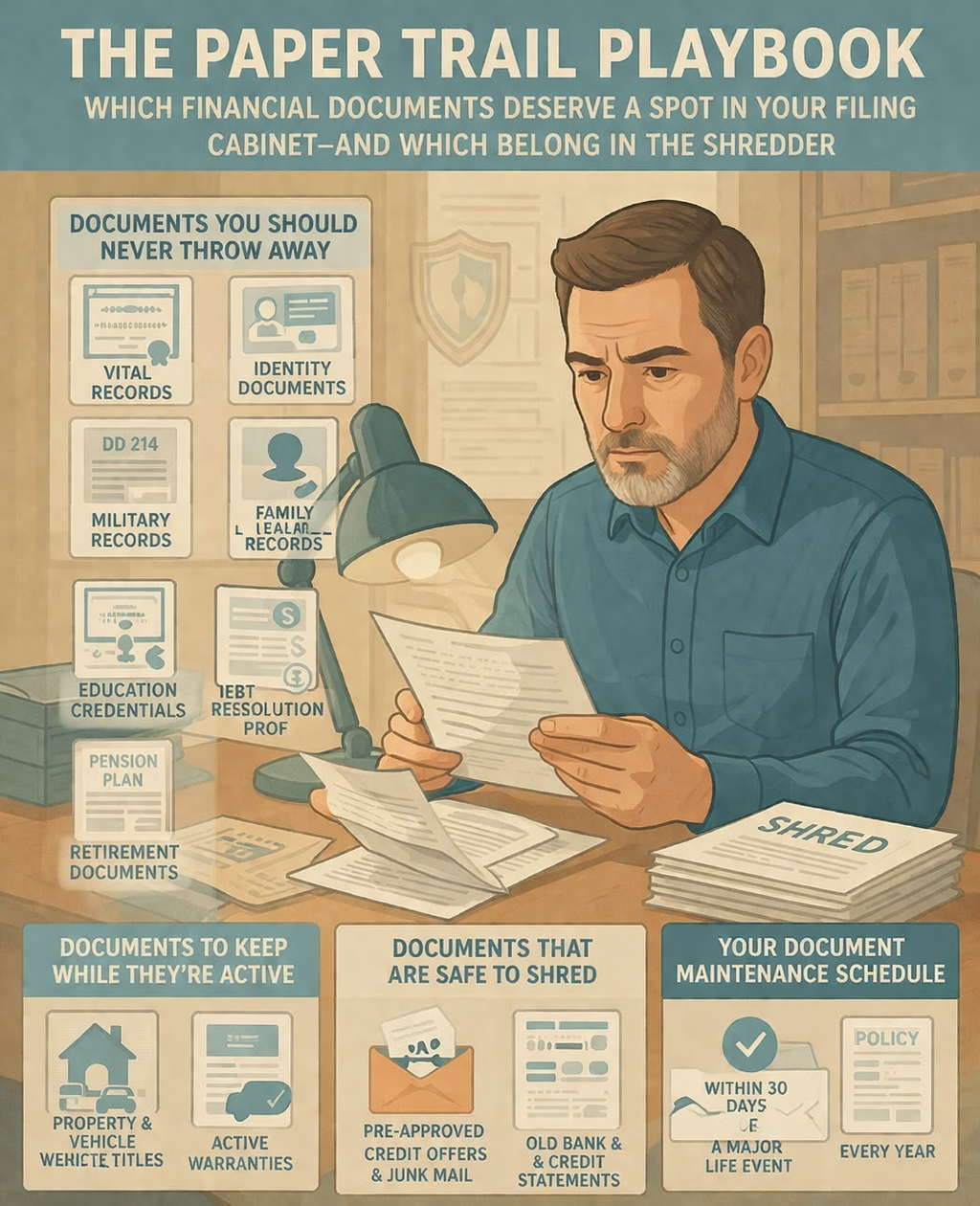

Documents You Should Never Throw Away

Certain records are irreplaceable or extremely difficult to obtain again. These belong in a fireproof safe or secure digital vault—permanently:

- Vital records — birth certificates, marriage licenses, death certificates

- Identity documents — Social Security cards, naturalization or citizenship papers

- Military records — discharge papers (DD-214)

- Family legal records — finalized divorce decrees, adoption papers, legal name change orders

- Education credentials — diplomas, transcripts, professional certifications

- Debt resolution proof — loan payoff confirmations and satisfaction letters

- Retirement documents — pension plan paperwork and benefit statements

- Medical documentation — bills and receipts that may support future tax deductions

These documents form the backbone of your personal and financial identity. Losing them can create significant headaches with government agencies, insurers, and financial institutions.

Documents to Keep While They're Active

Some paperwork matters only as long as the underlying asset or agreement is in play. Hold onto these for as long as you own the property, maintain the policy, or operate the business:

- Property and vehicle titles — deeds, car titles, boat registrations

- Active warranties — along with receipts for major home improvements or repairs

- Business formation documents — articles of incorporation, partnership agreements, operating agreements

- Insurance policies — even canceled ones, since past policies can be relevant if a claim surfaces later

Once the asset is sold, the warranty expires, or the business dissolves, you can reassess whether these still need to take up space.

Documents That Are Safe to Shred

If you're holding onto any of the following, it's time to fire up the shredder:

- Pre-approved credit offers and junk mail that contain personal details

- Old bank and credit card statements — unless you need them to support a tax filing, warranty claim, or billing dispute

- Tax returns older than seven years — the IRS statute of limitations generally covers this window

- Expired driver's licenses and ID cards

- Lapsed warranties and manuals for appliances or electronics you no longer own

- Travel documents — boarding passes and itineraries from completed trips

- Investment account statements older than one year — your annual summary captures the essentials

- Utility bills past one year — unless required for tax purposes or proof of residency

- Pay stubs — once you've verified them against your annual W-2

Important: Always shred rather than simply toss documents containing account numbers, Social Security digits, or other sensitive information.

Your Document Maintenance Schedule

Keeping the right paperwork isn't a one-time task, it requires periodic check-ins. Here's a simple cadence to follow:

Within 30 Days of a Major Life Event

Life changes like marriage, divorce, the birth or adoption of a child, a death in the family, a career move, or a relocation to a new state should trigger an immediate review of:

- Estate planning documents (wills, trusts, powers of attorney)

- Beneficiary designations on life insurance, annuities, 401(k)s, and IRAs

- Legal settlement paperwork

- Property titles and deeds

Every Year

Set an annual date, maybe around tax time, to review:

- Active insurance policies and annuity contracts

- Allocation options on any fixed index annuities

- Annual account summaries for annuities and retirement plans

- Investment account statements and transfer-on-death (TOD) designations

- Your Social Security statement

- Personal medical records, especially if managing chronic conditions or planning for long-term care

- Health care directives and living wills

- Digital account passwords and access instructions for your executor or trusted contact

Every 3–5 Years

Step back and evaluate the bigger picture:

- Whether your insurance coverage still matches your needs

- Whether your estate plan and beneficiary designations reflect your current wishes

Every 7–10 Years

Take a long-range view of your retirement strategy:

- Evaluate income options on fixed index annuities. Timing and suitability can shift as you age

- Reassess your overall retirement income plan

Everyone's situation is a little different, so the guidelines above are a starting point. If you'd like a personalized review of your financial documents and how they fit into your broader retirement plan, we're here to help.

Have questions? Reach out to schedule a conversation.

This blog offers general informational guidance and is not intended as tax, legal, or financial advice. Please consult with a qualified professional regarding your specific circumstances and document retention requirements.