What the Academic Research Really Says About Guaranteed Lifetime Income

03-14-2026

By Steve Gibson

How Income Riders Actually Work

An income rider (also called a Guaranteed Lifetime Withdrawal Benefit, or GLWB) is an optional feature attached to a fixed indexed annuity. It guarantees you a specific amount of income every year for life, regardless of what happens in the markets or how long you live.

There are two key components that determine your payout:

The Income Base — This is a tracking value (not your actual account balance) that grows during the deferral period. Many contracts offer a guaranteed rollup rate, often 6–8% simple or compound, that increases the income base every year you defer. Some contracts also offer “step-ups” that lock in any market gains above the guaranteed rollup.

The Distribution Rate — This is the percentage of your income base you receive annually for life. It increases with age. A typical contract might pay 4.5% at age 60, 5% at 65, 5.5% at 70, and so on.

This creates a powerful compounding effect when you defer: every year of deferral, your income base is growing AND you’re aging into a higher distribution rate. The result is a significantly larger guaranteed paycheck for life.

The Math:

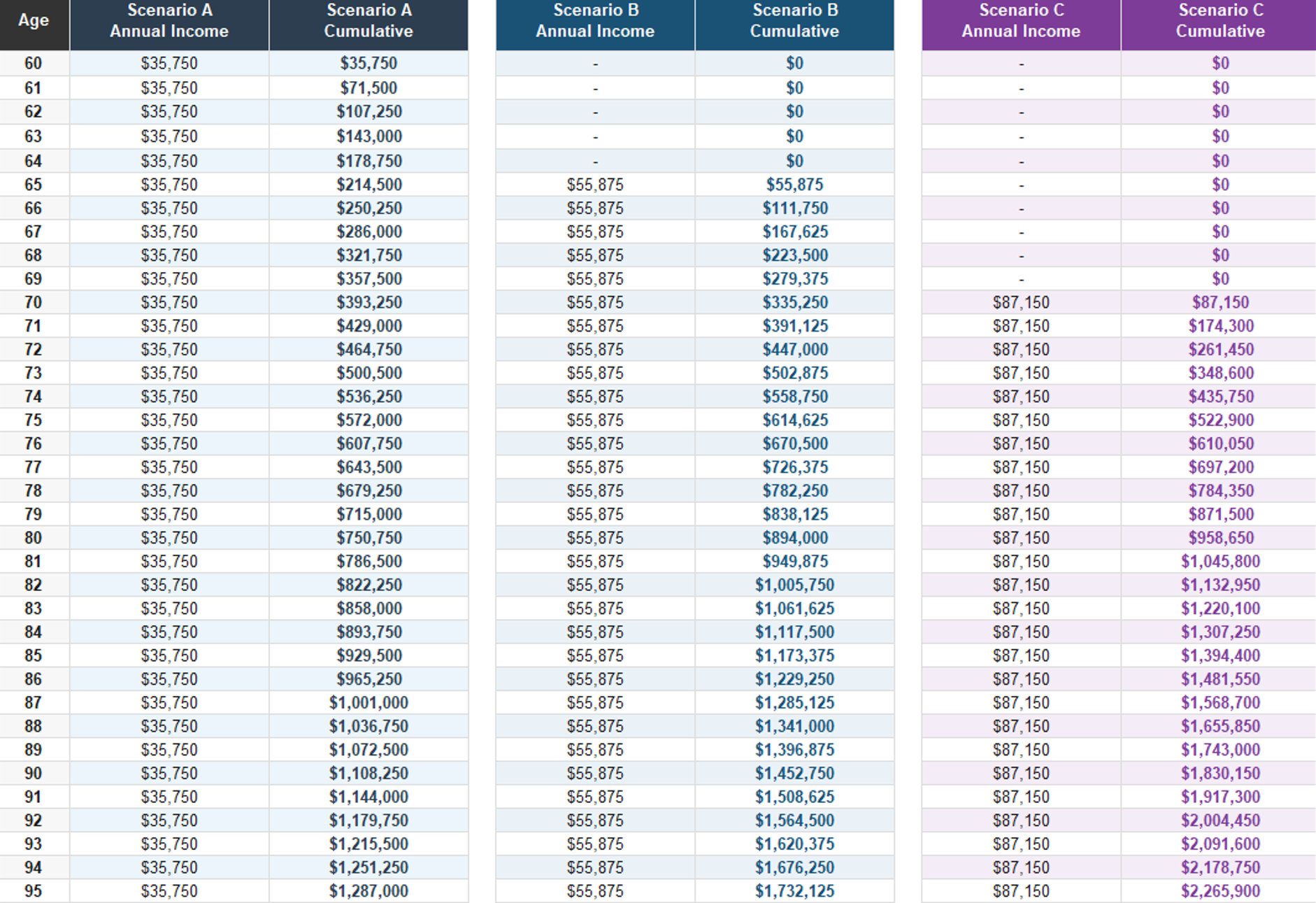

Let’s walk through a concrete example. A 60-year-old client places $500,000 into a fixed indexed annuity.

Scenario A — Immediate Activation (Age 60)

Annual Guaranteed Income: $35,750/year ($2,979/month)

Scenario B — Defer 5 Years (Activate at Age 65)

Annual Guaranteed Income: $55,875/year ($4,656/month)

Scenario C — Defer 10 Years (Activate at Age 70)

Annual Guaranteed Income: $87,150/year ($7,262/month)

By deferring 10 years, this client more than doubled their guaranteed lifetime income — from $35,750 to $87,150 per year. That’s an additional $51,400 every single year for the rest of their life. And this payout is guaranteed regardless of market performance.

Below is a chart to see visually see starting income now, waiting 5 years, and waiting 10 years.

What the Academic Research Says

This isn’t just financial planning theory. The strategy of combining guaranteed income floors with deferred activation is backed by decades of rigorous academic economics. Here’s what the leading researchers have found.

Wade Pfau, Ph.D. — The Income Floor

Pfau is a professor of retirement income at The American College of Financial Services and one of the most published researchers in this space. His “Safety-First” framework argues that retirees should build a guaranteed income floor to cover essential expenses before taking any market risk with remaining assets.

His research on the “Final Frontier” of retirement income demonstrates that portfolios combining annuities with living benefits (including income riders) alongside equities can reduce the risk of spending shortfalls by significant margins compared to an all-investment approach. In one analysis, a 100% stock portfolio left a 43.8% shortfall risk through age 100. Adding a GLWB-based annuity dramatically reduced that risk while still preserving meaningful legacy value.

In co-authored research with Michael Finke, Pfau also showed that deferred income annuities purchased before retirement can lower the total cost of funding retirement by cushioning both longevity risk and sequence-of-returns risk, the risk that a market downturn early in retirement permanently damages your portfolio.

Moshe Milevsky, Ph.D. — Mortality Credits and Longevity Risk Pooling

Milevsky, a finance professor at York University’s Schulich School of Business, has spent his career studying the mathematics of longevity risk. His central insight: when you pool resources with other retirees through an annuity, you earn what he calls “mortality credits”, an implicit return that no conventional investment can replicate.

Milevsky’s research shows that these mortality credits become more valuable the longer you defer. At younger ages, mortality credits are relatively small because few people in the pool are dying. But as you age, the credits compound. He has documented an implicit return from risk pooling of approximately 8% in a fixed-income context for older retirees, a return unavailable from any bond, CD, or traditional investment.

The practical takeaway: the longer you let your income rider defer, the more mortality credits are working in your favor, boosting the payout the insurance company can guarantee you.

David Blanchett, Ph.D. & Michael Finke, Ph.D. — The Value of the Guarantee

Blanchett, head of retirement research at PGIM, and Finke, professor of wealth management at The American College, have co-authored extensive research on GLWBs. Their work demonstrates that the guarantee itself has measurable economic value, especially during market downturns.

Their analysis shows that without a guarantee, a retiree who experiences a 20%+ market decline early in retirement faces severe pressure to cut spending. With a GLWB, the income floor holds firm. Blanchett’s research also found that the guaranteed distribution factor increasing with age is a critical design feature, it rewards patience by building deferral directly into the product’s payout structure.

Blanchett has further demonstrated that delaying Social Security should be considered first as a guaranteed income strategy, and that private annuity income riders serve as a powerful complement to fill the remaining income gap.

Roger Ibbotson, Ph.D. — FIAs as a Bond Alternative

Ibbotson, a Yale professor emeritus and creator of the iconic Stocks, Bonds, Bills, and Inflation chart, published landmark research in 2018 on fixed indexed annuities. His team at Zebra Capital Management simulated FIA performance from 1927 to 2016 and found that FIAs produced an annualized net return of 5.81% versus 5.32% for long-term government bonds, with comparable volatility but superior downside protection.

This matters for income rider deferral because during the deferral period, the underlying FIA is accumulating value through index-linked crediting strategies while your income base is growing through the guaranteed rollup. Ibbotson’s research validates that the FIA chassis itself is a sound accumulation vehicle, particularly in environments where bond returns are expected to be low.

His earlier monograph with the CFA Institute, “Lifetime Financial Advice: Human Capital, Asset Allocation, and Insurance,” argued that annuities should be a standard part of lifecycle financial planning. not an afterthought.

Robert Merton, Ph.D. — Think Income, Not Wealth

Robert Merton won the Nobel Prize in Economics in 1997. His contribution to retirement planning is deceptively simple but profound: stop measuring retirement success by the size of your portfolio. Measure it by the income it produces.

Merton’s framework divides retirement needs into three tiers. The first tier is your “floor”, guaranteed, inflation-protected income that covers essential expenses for life. Sources include Social Security, pensions, and lifetime income annuities. The second tier is conservative supplemental income. The third is aspirational spending funded by riskier growth assets.

Income riders fit squarely into Merton’s first tier. And his research makes it clear: you should secure the floor first. Only after guaranteed income covers your essentials should you take market risk with the rest. Deferring the income rider to build a larger guaranteed payout directly strengthens that floor.

Steve Vernon, FSA — Retirement Income Optimization

Vernon, a Fellow of the Society of Actuaries and research scholar at the Stanford Center on Longevity, has published extensive work on how retirees should generate income. His “Spend Safely in Retirement” strategy emphasizes maximizing guaranteed income sources first, particularly Social Security deferral and annuitization.

Vernon’s research aligns with the income rider deferral strategy: the longer you can fund expenses from other sources while your guaranteed income base grows, the larger your eventual lifetime paycheck. He frames it as a simple actuarial truth, insurance companies can afford to pay you more when you give them more time, because fewer people in the risk pool will collect.

Larry Kotlikoff, Ph.D. — Consumption Smoothing

Kotlikoff, a Boston University economics professor, developed the concept of “consumption smoothing”, the idea that your standard of living should remain as consistent as possible throughout your lifetime. His research demonstrates that most Americans either overspend early in retirement or underspend out of fear, and both outcomes reduce lifetime well-being.

Income riders support consumption smoothing by removing the guesswork. When you know exactly how much guaranteed income you’ll receive for life, you can plan your spending with confidence. Deferral enhances this by creating a larger, more stable income stream that better matches your actual living expenses in your later years, when healthcare costs typically rise and the ability to earn supplemental income declines.

Who Should Consider Deferral?

Not everyone should defer. The right strategy depends on your specific situation. Deferral makes the most sense if you have other income sources (Social Security, pension, part-time work, portfolio withdrawals) that can cover your expenses during the deferral period. It also makes sense if you’re in good health and want to maximize your income in later years when expenses tend to rise. And it’s ideal if you want the largest possible guaranteed income floor.

Immediate activation makes sense if you need income now, if you have limited other income sources, or if health concerns make a longer deferral impractical.

The beauty of the income rider is the flexibility: you choose when to activate it based on your life, not a pre-set schedule.

The Bottom Line

The academic consensus is clear: guaranteed lifetime income is one of the most efficient tools in retirement finance. From Pfau’s safety-first framework to Milevsky’s mortality credits, from Merton’s income-first approach to Kotlikoff’s consumption smoothing, the research converges on the same conclusion.

If you can afford to wait, deferring your income rider activation is one of the simplest, most mathematically sound decisions you can make in retirement planning. Two forces work in your favor simultaneously: your income base grows through the guaranteed rollup, and your distribution rate increases with age. The result is a significantly larger paycheck for life.

At Gibson Capital, we help clients design income strategies that align with their specific retirement timeline. Whether you need income today or want to maximize your payout through strategic deferral, we build the plan around your life, not around a product.

Academic References

Pfau, W. (2023). “Supporting Client Goals in Retirement: The Role of Structured Annuities with Living Benefits.”

Finke, M. & Pfau, W. (2015). “Reduce Retirement Costs with Deferred Income Annuities Purchased Before Retirement.” Journal of Financial Planning, 28(7): 40–49.

Milevsky, M.A. (2020). “Swimming with Wealthy Sharks: Longevity, Volatility and the Value of Risk Pooling.” Journal of Pension Economics & Finance, 19(2): 217–246.

Blanchett, D. & Finke, M. (2022). “Is a Guaranteed Lifetime Withdrawal Benefit Worth It?” Kiplinger.

Ibbotson, R. et al. (2018). “Fixed Indexed Annuities: Consider the Alternative.” Zebra Capital Management.

Ibbotson, R. et al. (2007). “Lifetime Financial Advice: Human Capital, Asset Allocation, and Insurance.” CFA Institute Research Foundation.

Merton, R.C. (2014). “The Crisis in Retirement Planning.” Harvard Business Review.

Merton, R.C. & Muralidhar, A. (2020). “SeLFIES: A New Pension Bond and Currency for Retirement.” SSRN Working Paper.

Vernon, S. (2017). “Spend Safely in Retirement.” Stanford Center on Longevity.

Kotlikoff, L. & Spivak, A. (1981). “The Family as an Incomplete Annuities Market.” Journal of Political Economy, 89(2): 372–391.

Disclosure: This material is for informational purposes only and does not constitute financial, tax, or legal advice. Annuity guarantees are backed by the financial strength and claims-paying ability of the issuing insurance company. Past performance is not indicative of future results. The hypothetical examples shown are for illustrative purposes only and do not represent any specific annuity product. Actual income rider features, rollup rates, and distribution percentages vary by product and carrier. Consult a qualified financial professional before making any financial decisions.