When Should You Claim Social Security? Here's What You Actually Need to Know

02-27-2026

By Steve Gibson

If you're 62 or older, figuring out when to claim Social Security is one of the most important financial decisions you'll face. Get the timing right, and it can meaningfully boost your retirement income for the rest of your life, and protect your spouse financially too. Get it wrong, and you could be leaving significant money on the table for decades.

What's making this decision even harder right now? A growing wave of anxiety about whether Social Security will actually be around, and it's pushing more and more people to file early, sometimes at a steep long-term cost.

The Rush to File Early — By the Numbers

For years, the trend was clear: older Americans were waiting longer to claim benefits. That trend has now reversed.

According to the Urban Institute, a Washington, D.C. think tank, Social Security applications rose by more than 276,000 from October 2024 through April 2025 compared to the same period a year earlier. Filings were on track to rise 15% for the fiscal year ending September 30.

And it wasn't just lower-income Americans leading the charge. Social Security data for the first half of fiscal 2025 showed that the agency received more early claims from higher earners too, not just those who needed the income right away.

The pace did cool off somewhat. Filings rose 8% for the full calendar year 2025, still a dramatic jump compared to 2024, when the number of people who filed rose just 1.8%.

So what's driving it?

"We may be seeing more of a generalized anxiety over the health of Social Security. Some people are choosing to file early because they're concerned about the state of the program going forward." — Jack Smalligan, Senior Policy Fellow, Urban Institute

A recent AARP survey backs that up. Roughly half of Americans who claimed earlier than planned in the past year, or are considering doing so, said they were motivated by fears that Social Security is running out of money.

Other contributing factors include persistently high inflation squeezing retirees' budgets and a peak wave of baby boomers hitting retirement age all at once.

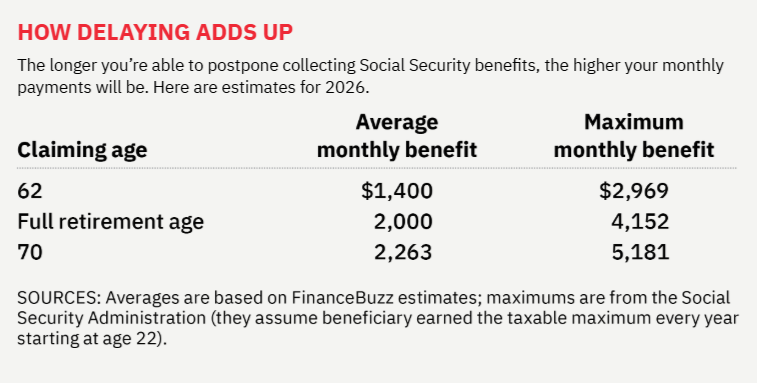

The Real Payoff for Waiting

Let's start with the basics, because they matter more than most people realize.

You can file as early as age 62. But doing so will reduce your monthly payout by up to 30% compared to what you'd receive at your Full Retirement Age (FRA):

- FRA is 66 for people born in 1943

- It gradually increases to 67 for those born in 1960 or later

Waiting until your FRA also maximizes your annual cost-of-living adjustment (COLA), since that percentage increase gets applied to a larger base amount each year, the power of compounding working in your favor.

Can You Change Your Mind?

Yes, but only within the first 12 months after filing. During that window, you can withdraw your claim, repay the benefits you've already received, and refile later. After that first year, the decision is permanent.

What If You Keep Working?

If you file before your FRA and continue working, Social Security will withhold $ 1 for every $2 you earn over a certain annual threshold. In 2026, that threshold is $24,480.

In the year you actually reach your FRA, the withholding drops to $1 for every $3 you earn over $65,160(the 2026 limit). Once you hit FRA, the earnings test disappears entirely, and Social Security will recalculate your benefit to credit you for the amounts previously withheld.

The Case for Waiting Even Longer

If you can delay past your FRA, you'll earn an 8% delayed-retirement credit for each year you wait, up to age 70.

For workers whose FRA is 67, waiting until 70 means a 24% increase in benefits. A study by the National Bureau of Economic Research found that "virtually all" workers between ages 42 and 62 would end up with higher lifetime discretionary spending by waiting until at least 65 to file, and 90% would benefit by waiting until 70.

Let's Talk About the Insolvency Fear

Here's where a lot of people go wrong.

Nearly 30% of Social Security recipients elect to take benefits at age 62, while only 10% wait until 70, according to a 2024 study by the Bipartisan Policy Center.

Fear of the program going broke is a big part of that.

But here's the thing. That fear, while understandable, isn't a good reason to file early.

Yes, if Congress does nothing, the Social Security trust fund is projected to run out by 2034. But "running out" doesn't mean benefits stop. Social Security would still be funded by ongoing payroll taxes and would continue paying benefits, just reduced by roughly 23%. Experts broadly agree Congressional action is likely, given how politically popular the program is.

And here's the kicker: even if benefits were cut by 23%, you'd still be better off waiting. Any reduction gets applied proportionally, so a larger benefit still wins.

For example:

| Age 67 | Age 70 | |

|---|---|---|

| Before reduction | $2,000/month | $2,480/month |

| After 23% reduction | $1,540/month | $1,910/month |

"I'll Just Invest the Money Instead" — A Risky Strategy

Social media has been buzzing lately with a tempting idea: claim at 62 and invest the money to earn a better return than waiting would provide.

It sounds clever. In practice, it's a gamble.

To outpace both Social Security's annual COLA and the guaranteed 8% delayed-retirement credit, you'd need to invest very aggressively, something most retirees aren't positioned to do comfortably.

"Most retirees aren't going to be 100% in stocks." — Wade Pfau, Founder, RetirementResearcher.com

A 2023 paper in the Journal of Financial Planning by Pfau and Steve Parrish of The American College of Financial Services found that while delaying Social Security may mean giving up some upside in a roaring bull market, that scenario happens less often than many expect. And if the market drops early in retirement, what's called sequence-of-returns risk, retirees drawing down a stock-heavy portfolio could face permanent financial damage, dramatically increasing the risk of running out of money altogether.

Legitimate Reasons to File Before 70

To be clear: waiting until 70 isn't the right answer for everyone. Here are real reasons some people are better off filing earlier.

You Don't Like Watching Your Savings Shrink

For many retirees, filing early means they don't have to draw down their savings accounts. There's real psychological value in that.

You Want the Comfort of a Regular "Paycheck"

For retirees who don't receive a pension, Social Security can fill that role — providing steady, predictable income every month.

Your Health Isn't on Your Side

An analysis by J.P. Morgan Asset Management suggests the math breaks down roughly like this:

- Claim at 62 if you don't expect to live past 77

- Wait until your FRA if you expect to live beyond 77

- Wait until 70 if you expect to live beyond 81

That said, the Social Security Administration estimates that average life expectancy for a 65-year-old man is 84.3 years, and for a 65-year-old woman, it's 87 years, so statistically, most people benefit from waiting.

You Want to Leave an Inheritance

A Morningstar analysis found that retirees who delay Social Security by drawing from their portfolios end up with higher lifetime spending income, but a lower median portfolio balance when they die. If leaving money to your heirs is a priority, this trade-off matters.

What About Your Spouse?

This is where the conversation gets more nuanced, and more important.

If you're the higher earner in your household, your claiming decision doesn't just affect you. Once you pass away, your surviving spouse (assuming they've reached FRA) is entitled to up to 100% of your benefit, or 100% of what you would have received if you hadn't yet filed.

Survivor benefits are especially important when one spouse spent time out of the workforce, say, raising children. Since Social Security is based on your 35 highest-earning years, gaps in employment can significantly reduce one spouse's benefit. Switching to the higher earner's benefit could make a major difference in quality of life for the person left behind.

At the same time, waiting until 70 can create a cash flow problem for couples in the meantime. A practical solution:

One approach: have the lower-earning spouse file at FRA(or even as early as 62) to cover household expenses while the higher earner's benefit continues to grow.

Also worth knowing: spousal benefits allow a lower-earning spouse to receive up to half of the higher earner's FRA benefit — but only if the lower earner waits until their own FRA to file. Filing earlier reduces that spousal benefit.

The Bottom Line

There's no single right answer here. The best claiming age depends on your health, your finances, your spouse's situation, your other income sources, and honestly your peace of mind.

What shouldn't drive the decision is panic.

The math generally favors waiting, especially if you're in good health, have a younger spouse, or want to maximize your inflation-protected income in your later years. But life isn't always lived on a spreadsheet.

Talk to a financial planner who can look at your full picture. Ask the hard questions about your health, your goals, and what you actually want retirement to look like. Then make the call that's right for you, not one driven by headlines or social media hot takes.

This post is for informational purposes only and does not constitute financial advice. Please consult a qualified financial professional before making Social Security claiming decisions.